The Expansion of AIF Universe in India

Sophisticated investors investing in India are no longer required to settle for the fund. Increasingly, they want the deal, i.e., the specific, high-conviction opportunity sitting inside the fund’s portfolio. The shift of interest in investors is reshaping the Alternative Investment Fund (“AIF”) universe in India and two regulators would need to be considered: Securities Exchange Board of India (“SEBI”) on the securities side, and Reserve Bank of India (“RBI”) on the foreign exchange side.

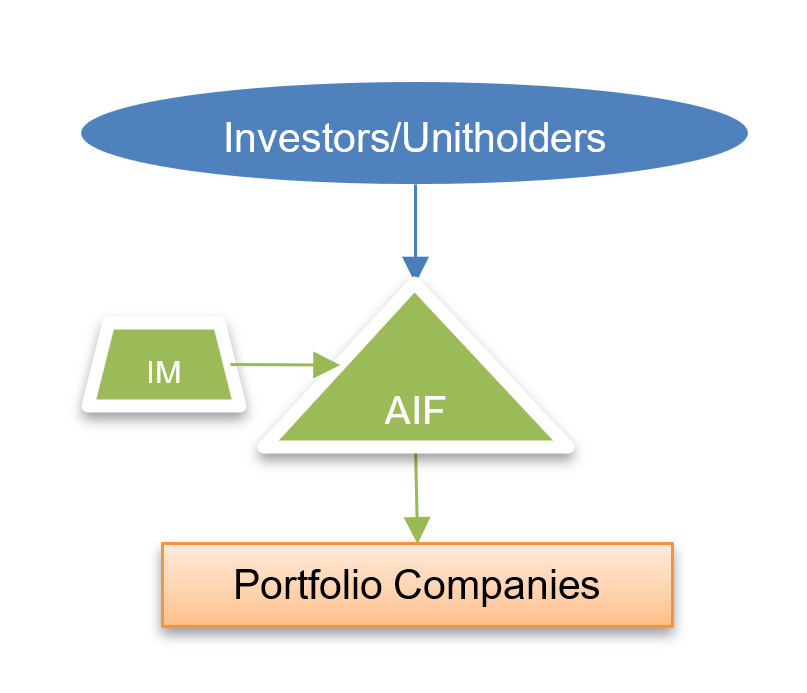

An AIF is a privately pooled investment vehicle that can be structured as a company, limited liability partnership (“LLP”) or trust. AIFs aggregate capital from investors specifically high net worth individuals (“HNIs”) and institutional investors, both resident in India and based outside India, to deploy into various asset classes. Governed by the SEBI (Alternative Investment Funds) Regulations, 2012 (“AIF Regulations”), the investment manager (“IM”) exercises discretion over where and when to deploy the capital, while investors, as limited partners (“LPs”), reap benefits from the pooled strategy.

While that was the case until recently, a new generation of accredited investors (“AIs”), resident and non-resident alike, want more. Regulatory developments in 2025 now give them exactly that: the ability to co-invest directly alongside the AIF into specific portfolio companies, on a deal-by-deal basis, with concentrated exposure and streamlined compliance.

For LPs based outside India, whether Singapore-domiciled VC funds, Cayman-structured family offices or non-resident indians, the new co-investment structures (Co-investment Vehicle Schemes (“CIVs”) and Accredited Investor-only Schemes (“AI-only Schemes”)) carry a second regulatory layer that domestic LPs do not face: the Foreign Exchange Management Act, 1999 (“FEMA”) and India’s Foreign Direct Investment (“FDI”) framework. When a foreign LP co-invests through a CIV directly into a portfolio company, that investment is not a passive fund unit subscription, it is a standalone equity investment into an Indian company, with all the attendant FEMA obligations: sectoral caps, pricing guidelines, entry route compliance, and RBI reporting.

This article maps both layers, SEBI’s new co-investment architecture introduced in 2025 through amendments to the AIF Regulations, and the FEMA framework that foreign LPs must navigate to give practitioners a consolidated brief on what has changed and what it means in practice.

AIF Landscape in India CY 2025

| Particulars | Cumulative Figures as of Dec 2025 | For CY 2025 |

| Total Commitments | ~INR 15.74 Trillion [c. USD 175 Bn] | ~ INR 2.69 Trillion |

| Total Funds Raised | ~INR 6.79 Trillion [c. USD 75.41 Bn] | ~ INR 1.52 Trillion |

| Total Investments made by AIFs | ~INR 6.45 Trillion [c. USD 72 Bn] | ~ INR 1.39 Trillion |

| No. of AIFs in India | 1,700 | ~ 276 |

Source: (1) SEBI – Data relating to activities of Alternative Investment Funds (AIFs) www.sebi.gov.in/statistics/1392982252002.html

(2) Address by SEBI Chairman on 11 March 2026 at IVCA Conclave 2026 – The Evolving Agenda for Alternative Investment Funds

(3) SEBI reports and statistics bulletin for January 2025 https://www.sebi.gov.in/sebi_data/commondocs/jul-2025/SEBI_Bulletin_January_2025%20Excell_p.xlsx and for January 2026 https://www.sebi.gov.in/sebi_data/commondocs/jan-2026/Annexure%20Tables%20January%202026_p.xlsx

What purpose does AIF serve?

- Gather capital from a sophisticated class of investors, domestic or international,

- for deployment based on a defined investment strategy of the IM;

- focusing on specific asset classes not accessible through traditional investment options;

- to provide enhanced returns for investors.

What alternative strategies have emerged as a result of AIF model in India?

Co-investing: AIF would invest the pooled capital from investors into a portfolio company as per the investment strategy. Co-investment would permit an investor to simultaneously invest money into such portfolio company alongside the AIF. This provides such investors (who are already investors in the AIF) a chance to maximize exposure to certain asset classes without going through the AIF path for such investments.

Illustratively, if a SEBI-registered Category II AIF led by a prominent VC firm invests INR 500 million in a high-growth Series B fintech startup, an accredited investor who has already committed INR 100 million to that AIF may co-invest an additional INR 300 million directly into the same startup via a CIV Scheme thereby, gaining concentrated, high-conviction exposure to a specific bet, without altering the main fund’s pooled strategy or diluting returns for other investors.

Investors have found a way to enhance wealth by co-investing alongside AIF in select portfolio companies selected by the IM. In a way, they are making better use of the investment strategy and investment expertise of the IM for their own personal wealth maximization.

How is co-investment currently governed?

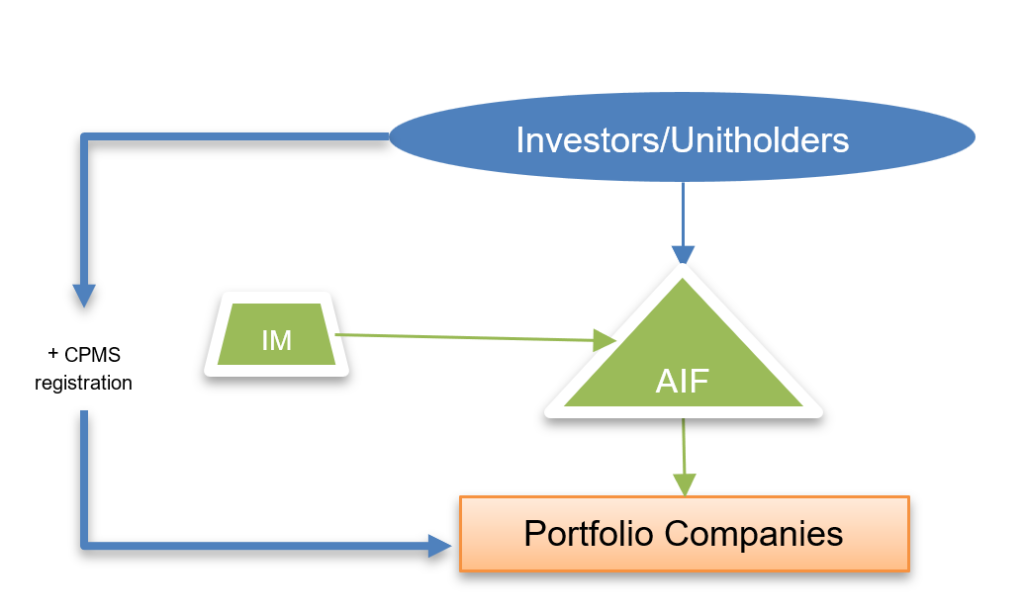

Through the SEBI (Portfolio Managers) (Fourth Amendment) Regulations, 2021, which has come into effect on 8 December 2021, amended the SEBI (Portfolio Managers) Regulations, 2020 (“PMS Regulations”), co-investment was introduced as an option for AIF investors under the Portfolio Management Services (“PMS”) route. It is governed by the PMS Regulations.

How is the PMS route placed in the AIF structure?

The 2021 amendment to the PMS regulations enabled co-investment in unlisted securities to the investors through the Portfolio Management Service (“CPMS”) route. Co-investment Portfolio Managers were required to be registered with SEBI to offer their services.

Has there been any update to this PMS route?

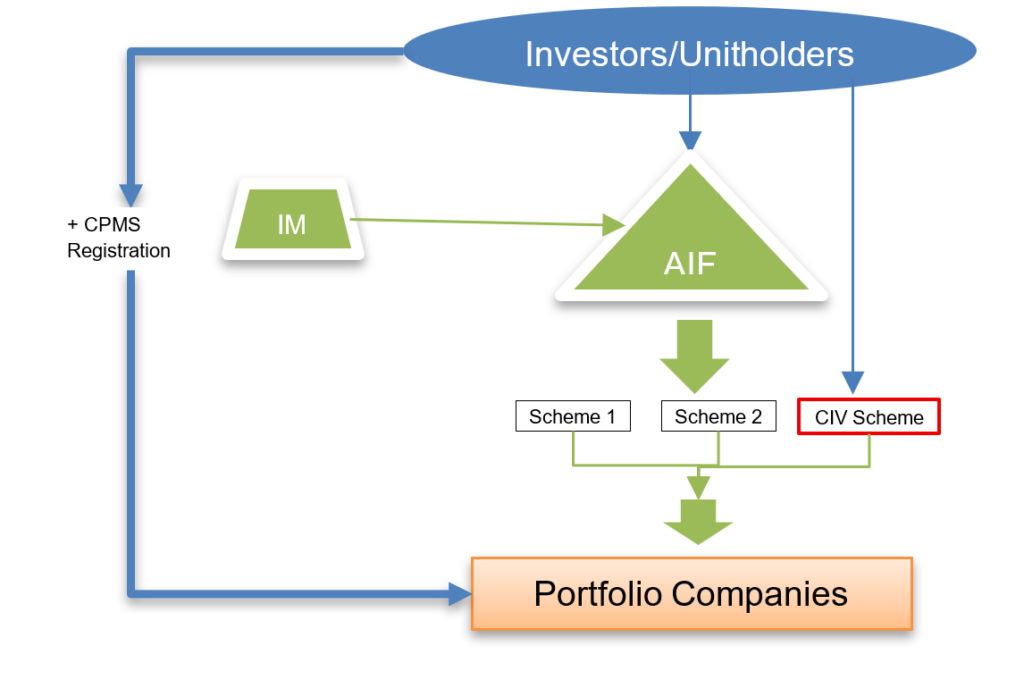

Recently, in 2025, the AIF regulations were amended to state that Category I and II AIFs are permitted to facilitate co-investments directly through the creation of a Co-investment Vehicle Scheme (“CIV/CIV Scheme”) within the existing AIF structure. The CIV acts as a streamlined, low-compliance alternative to the traditional PMS route.

Unlike a general fund pool, each CIV, within an existing AIF, is established as a distinct, ring-fenced scheme dedicated to a specific investment opportunity. This structure mandates absolute segregation of bank accounts, demat accounts, and assets to ensure that co-investor capital remains shielded from the liabilities or performance of the primary AIF or other parallel CIV schemes.

There is a cap on the standard investor’s CIV contribution at three times their exposure in the main fund to any specific portfolio company.

Is the CIV route open for all investors of AIF?

To ensure that this high-concentration route is reserved for those capable of absorbing its unique risks, participation through CIV route is strictly limited to Accredited Investors (“AIs”). AIs are high-net-worth individuals or entities who meet specific financial thresholds and have obtained formal certification from an accreditation agency. By restricting the CIV route to this class of investors, the regulator balances the demand for “high-conviction” deal access, with the necessity of robust investor protection. This dual system, where CIVs exist alongside within an AIF but do not replace the existing PMS route (governed by the PMS regulations), provides fund managers with a versatile toolkit to meet the diverse liquidity and exposure needs of their most sophisticated clients.

Who Qualifies as an Accredited Investor?

| Investor Category | Financial Threshold (Any One) | Certificate Required? | Validity |

| Individual / HUF / Family Trust / Sole Proprietorship | Annual income ≥ INR 2 crore; OR Net worth ≥ INR 7.5 crore (of which ≥ INR 3.75 crore in financial assets); OR Annual Income ≥ INR 1 crore + Net worth ≥ INR 5 crore, out of which atleast INR 2.5 crore is in form of financial assets. | Yes | 1 year (2 years if criteria met for preceding 3 years) |

| Body Corporate | Net worth ≥ INR 50 crore | Yes | 1 year (2 years if criteria met for preceding 3 years) |

| Trusts (other than family trusts) | Assets under Management ≥ INR 50 crore | Yes | 1 year (2 years if criteria met for preceding 3 years) |

| Partnership Firm | Each partner must independently meet the individual threshold | Yes | 1 year (2 years if criteria met for preceding 3 years) |

| Foreign Investor (NRI / Foreign Entity) | Same thresholds as applicable category above, assessed on INR-equivalent of foreign income / net worth | Yes | 1 year (2 years if criteria met for preceding 3 years) |

| Deemed Accredited Investors | Central / State Governments; developmental agencies / funds set up by them; QIBs; Category I FPIs; Sovereign Wealth Funds; Multilateral Agencies (e.g. World Bank, ADB, IFC, IMF) | No certificate required as deemed by regulation |

Source: Reg. 2(1)(ab), SEBI (AIF) Regulations, 2012;

Further, an AIF can offer Accredited Investor-only schemes (AI-only Schemes) under the CIV route.

So how exactly is a CIV any different from the existing PMS Route?

| Parameter | CPMS Route (2021) | CIV Route (2025) |

| Purpose | To enable Managers of AIFs to offer co-investment in unlisted securities to their investors through the PMS route | Addressed issues of compliance costs arising from separate PMS registration to be obtained by portfolio managers |

| Registration | Separate PMS registration with the SEBI required to be obtained by portfolio managers | Integrated within AIF structure |

| Investor Eligibility | Open to all AIF investors | Accredited investors only |

| Investment Cap | No specific cap | 3× investor’s contribution by the investor in the main AIF |

| Terms Parity | Must match main terms of AIF | Cannot be more favorable than main AIF |

| Exit Timeline | Must align with main fund | Must align with main fund |

| Compliance | Full PMS obligations | Streamlined AIF documentation |

| Status | Available since 2021 | Available since September 2025 |

| Best For | Non-accredited investors Large co-investments |

Accredited investors Simplified operations |

What are AI-only Schemes?

The SEBI (AIF) Third Amendment Regulations, notified on 18 November 2025, formally integrated Accredited Investor-only Schemes (“AI-only Schemes“) into the AIF Regulations. AI-only Schemes are permitted to offer differential rights and benefits to specific investors. While standard AIF schemes are generally limited to 1,000 participants (a cap that applies specifically to non-accredited investors), AI-only Schemes have no upper limit on the number of investors who can participate schemes enjoy greater operational longevity. While conventional AIFs are typically restricted to a 2-year extension period, AI-only Schemes can extend their tenure by up to 5 years, provided they secure the necessary investor consent.

AI-only Schemes: New Privileges

| Parameter | Regular AIF Schemes | AI-only Schemes |

| Introduction | Existed before 2025 | Introduced November 2025 |

| Pari-Passu Rule | Mandatory equal treatment | Can offer differential rights |

| Differential Rights | Only Large Value Funds (LVFs*) could differentiate | Full flexibility for all AI-only schemes |

| Investor Cap | Max 1,000 investors (non-accredited) | NO UPPER LIMIT |

| Fund Tenure Extension | 2 years (with consent) | 5 years (with consent) |

| Investor Requirement | Mixed allowed | 100% accredited mandatory |

*LVF is defined under Regulation 2(1)(pa) of AIF regulations as an AIF or scheme of an AIF in which each investor is an accredited investor and invests not less than INR 250 million in such AIF.

What is the growth in Accredited Investor (AI) population?

The most dramatic pattern following the 2025 amendments has been the surge in AIs, directly driven by the new requirements for CIVs, Angel Funds, and AI-only schemes.

| Period | Accredited Investors | Growth |

| May 2025 | 649 | Baseline |

| February 2026 | 2,181 | +236% in 9 months |

| Market Share | 30% of total AIF investments | Significant concentration |

Source: Address by SEBI Chairman on 11 March 2026 at IVCA Conclave 2026 – The Evolving Agenda for Alternative Investment Funds https://www.sebi.gov.in/media-and-notifications/speeches/mar-2026/address-by-shri-tuhin-kanta-pandey-chairman-sebi-at-the-ivca-conclave-2026_100233.html

What is the taxation framework governing CIVs?

Currently, the Income-tax Act, 2025 (“IT Act”) has not provided any express provisions regarding the taxation of CIVs.

Since CIVs may be constituted only by Category I and Category II AIFs (refer Regulation 17A read with Regulation 2(1)(fa) of the SEBI (Alternative Investment Funds) Regulations, 2012, as amended), and is a scheme within the AIF rather than a separate legal fund, it is possible to take a view that the taxation applicable to a CIVs shall align with the tax treatment applicable to Category I and Category II AIFs. One will have to revisit the tax position if the Government provides any subsequent clarification / changes in the IT Act in this regard.

Taxation of Category I and II AIFs

- Fund level taxation

Category I and II AIFs are granted “pass-through” status under Schedule V of the Income-tax Act, 2025 (“IT Act”) read with Section 11 (Section 10(23FBA) in the erstwhile Income-tax Act, 1961) and Section 224 of the IT Act (Section 115UB of the erstwhile Income-tax Act, 1961). This means that any income generated by the fund, excluding business income, is not taxed at the fund level. Instead, the tax liability flows directly to the investors, who are taxed as if they had made the investments themselves. Any business income of the fund is taxed at the vehicle level depending on whether it is incorporated as a trust, company or LLP.

- Investor/ Unit holder level taxation

Taxation at the investor / Unit holder level shall be as if they had made the investments themselves directly. Therefore, any capital gains/ dividend income earned by the AIF from its underlying investment shall be taxable in the hands of the Investor / Unit holder as below:

| Nature of Income | Resident Investors | Non-Resident Investors |

| Long-term capital gains on listed equity shares/ units of equity-oriented funds/ units of business trust exceeding one lakh twenty-five thousand rupees [Section 198 of the IT Act/ Section 112A of the Income-tax Act Tax, 1961] | 12.5% | 12.5% or such other lower rate as prescribed under the relevant DTAA, whichever is beneficial |

| Long-term capital gains on any other assets other than the above [Section 197 of the IT Act/ Section 112 of the Income-tax Act Tax, 1961] | 12.5% | 12.5% or such other lower rate as prescribed under the relevant DTAA, whichever is beneficial |

| Short-term capital gains on listed equity shares/ units of equity-oriented funds/ units of business trust [Section 196 of the IT Act/ Section 111A of the Income-tax Act Tax, 1961] | 20% | 20% or such other lower rate as prescribed under the relevant DTAA, whichever is beneficial |

| Short-term capital gains on any other assets other than the above | Applicable rates (Refer Note 2) | Refer Note 3 |

| Dividends and any other income in respect of securities | Refer Note 4 |

Note 1: The tax rates set out in the above table and notes below are exclusive of surcharge at applicable rates and health and education cess at 4% on the aggregate of tax and surcharge.

Note 2: Short-term capital gains (not governed by Section 196 of the IT Act), dividends and any other income in respect of securities arising to a resident investor shall be taxable at the applicable rates as follows:

- In the case of individuals – slab rates shall apply;

- In the case of domestic companies – 22% or 30% depending on the eligibility and option selected; and

- In the case of limited liability partnerships and partnership firms – 30%.

Note 3: Short-term capital gains (not governed by section 196 of the IT Act) arising to a non-resident investor shall be taxable at the applicable domestic rates or at such lower rate as prescribed under the relevant DTAA, whichever is beneficial. Where the non-resident investor qualifies as a Foreign Institutional Investor within the meaning of Section 210 of the IT Act [Section 115AD of the Income-tax Act, 1961], such gains shall be taxable at 30% or at such lower rate as may be prescribed under the relevant DTAA, whichever is beneficial.

Note 4: Dividends and any other income in respect of securities arising to a non-resident investor shall be taxable at the applicable domestic rates or at such lower rate as prescribed under the relevant DTAA, whichever is beneficial. Where the non-resident investor qualifies as a Foreign Institutional Investor within the meaning of Section 210 of the IT Act [Section 115AD of the Income-tax Act, 1961], such gains shall be taxable at 30% or at such lower rate as may be prescribed under the relevant DTAA, whichever is beneficial.

Note 5: On sale of units of an AIF by the Investor / Unit holder, it shall be taxable at the rate of 12.5% on long term capital gains and at applicable tax rates if it is short term capital gains as discussed above.

What has been the Market Response? Verified Data (2025-2026)

Overall Market Growth

| Metric | December 2025 | Growth Rate |

| Total Commitments | ₹15,740 billion | +20.6% YoY |

| Capital Raised | ₹6,780 billion | +28.7% YoY |

| Investments Made | ₹6,450 billion | +27.4% YoY |

| 5-Year CAGR | ~30% | Sustained growth |

Source: SEBI Data relating to activities of AIFs https://www.sebi.gov.in/statistics/1392982252002.html

Address by SEBI Chairman on 11 March 2026 at IVCA Conclave 2026 – The Evolving Agenda for Alternative Investment Funds https://www.sebi.gov.in/media-and-notifications/speeches/mar-2026/address-by-shri-tuhin-kanta-pandey-chairman-sebi-at-the-ivca-conclave-2026_100233.html

Accredited Investor Explosion

Category-Wise Performance

| Category | Commitments (Dec 2025) | YoY Growth |

| Category II (PE/VC/Credit) | ₹11,640 billion | +16.1% |

| Category III (Hedge Funds) | ₹1,960 billion | +43.3% |

| Category I (Angel/VC/Infra) | ₹980 billion | +15.5% |

Source: SEBI Data relating to activities of AIFs https://www.sebi.gov.in/statistics/1392982252002.html

Key Insight: Category III (hedge funds) showed fastest growth at 43.3%, benefiting most from AI-only scheme flexibility.

The Startup Funding Paradox

Despite explosive growth in AIF capital, SEBI has flagged a critical concern: minimal capital flowing to innovation and early-stage startups.

| Metric | Value |

| Total AIF Investments (Dec 2025) | ₹6,450 billion |

| Investment to Startups | ₹205 billion |

| Percentage to Startups | ~3.18% |

Source: Address by SEBI Chairman on 11 March 2026 at IVCA Conclave 2026 – The Evolving Agenda for Alternative Investment Funds https://www.sebi.gov.in/media-and-notifications/speeches/mar-2026/address-by-shri-tuhin-kanta-pandey-chairman-sebi-at-the-ivca-conclave-2026_100233.html

Key Patterns Identified

Pattern 1: Dual-Track Regulatory Architecture

SEBI is creating parallel routes (CIV vs CPMS, AI-only vs regular) rather than replacing old frameworks. This gives fund managers strategic choice based on investor composition.

Pattern 2: Accredited Investor Centralization

The most striking pattern is the systematic pivot toward accredited investors across all three amendments: CIVs require them, Angel Funds now exclusively serve them, and AI-only schemes offer privileges for them. 236% growth in 9 months confirms this is reshaping the market.

Pattern 3: Operational Flexibility Through Segregation

CIVs require deal-by-deal schemes with strict ring-fencing. Angel funds shifted to deal-by-deal consent. This prevents cross-contamination but increases structural complexity.

Pattern 4: The Compliance Trade-off

Lower entry barriers (removed ₹5 Cr corpus, lower minimums, shorter lock-ins) paired with new protective mechanisms (3× cap, mandatory ring-fencing, co-terminus exits). Ease of entry but prevent concentration risk.

Pattern 5: Category III Leadership

Hedge funds (Category III) showed 43.3% growth, fastest among all categories. They benefit most from AI-only scheme flexibility, suggesting investors value operational freedom.

Pattern 6: The Success Paradox

Amendments successfully mobilized massive capital, but it’s flowing to safety (private credit, real estate, late-stage PE) rather than innovation. Only 3.2% reaches startups.

What will be the implication of FEMA and FDI on Foreign LPs?

FEMA and FDI Implications for Foreign LPs: CIVs and AI-only Schemes

While SEBI governs fund registration and co-investment structures, RBI governs the movement of foreign capital in and out of India under FEMA, 1999, read with the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 (“NDI Rules”) and RBI’s Master Direction on Foreign Investment in India. For a foreign LP considering CIV co-investment or participation in an AI-only Scheme, SEBI accreditation is necessary but not sufficient, FEMA compliance is an independent, parallel obligation that cannot be contracted out of or waived off.

How AIFs Are Classified Under FEMA: The Investment Vehicle Framework

Under the NDI Rules, AIFs are considered as ‘Investment Vehicles’ and non-resident investors may invest in AIFs. When a non-resident LP invests in an AIF unit, that investment is in the AIF, not a direct equity investment in the AIF’s portfolio companies. This distinction is foundational: it is what makes pooled AIF investing relatively easier from a FEMA standpoint. The AIF holds the investment and sectoral cap compliance is managed at the fund level.

The critical FEMA question for CIVs and AI-only Schemes, however, is whether the AIF is classified as a Foreign Owned or Controlled Company (“FOCC”). The NDI Rules, as amended in August 2024, define “control” of an AIF as vesting in its sponsors and managers or investment managers. This means that even if 80% of the LP base is foreign, an AIF managed by an Indian IM is not a FOCC, its downstream investments are treated as domestic. Conversely, if a foreign entity controls the IM or sponsors the AIF, the fund is a FOCC, and every portfolio investment it makes (including through CIV Schemes) constitutes Indirect Foreign Investment (“IFI”) subject to full FDI compliance at the portfolio company level.

The CIV Problem: From Unit Subscription to Direct Equity

The CIV structure fundamentally changes the compliances required under FEMA. When a foreign LP invests in a CIV Scheme, that CIV makes a direct equity investment into the portfolio company. This is not a fund unit subscription; it is a standalone equity transaction. The guiding principle under FEMA is what cannot be done directly cannot be done indirectly. Accordingly, the CIV co-investment by a foreign LP is treated as direct FDI in the portfolio company and must comply with: (i) the applicable entry route (automatic or government approval); (ii) sectoral caps – which aggregate across all foreign investors in the portfolio company; (iii) pricing guidelines under the NDI Rules (fair market value for unlisted securities); and (iv) RBI reporting obligations. Each CIV deal is a distinct FEMA transaction, multiplying the compliance burden significantly compared to the pooled fund model.

The NRI/OCI Carve-out: A Planning Advantage

One significant planning opportunity exists for the NRI and OCI LP community. The August 2024 amendment to the NDI Rules extended an existing NRI carve-out to OCIs: investments made by an Indian entity owned and controlled by NRIs or OCIs on a non-repatriation basis in compliance with Schedule IV of the NDI Rules are not counted as Indirect Foreign Investment (“IFI”). This means that an NRI- or OCI-controlled fund investing in a CIV on a non-repatriation basis is treated as a domestic investor for the purposes of downstream investment classification. For this class of investors, the CIV route would have lesser compliances to abide by: no sectoral cap aggregation concerns at the portfolio company level. This is a meaningful structural advantage for NRI family offices and NRI-controlled investment vehicles considering CIV participation.

Sovereign Wealth Funds and DFIs: The Preferred Class

SEBI’s CIV circular already carves out sovereign wealth funds (“SWFs”), multilateral and bilateral Development Finance Institutions (“DFIs”), and government-controlled entities from the 3× investment cap. This exemption aligns neatly with the FEMA framework, which has historically provided a lighter regulatory touch for these categories of investors through Schedule VII of the NDI Rules for long-term investors. For foreign government-backed entities co-investing through CIVs, the combined effect is maximum flexibility no cap on co-investment quantum, and a more predictable FEMA pathway given their established reporting infrastructure. AIF managers targeting institutional co-investors should structure their Shelf PPMs with this class of LP explicitly in mind.

Prohibited Sectors and the Shelf PPM Gap

A significant gap exists in the current CIV framework: the SEBI circulars are silent on FDI-prohibited sectors. If a portfolio company operates in a sector where FDI is prohibited which includes certain real estate activities, gambling, chit funds, or sectors requiring prior government approval, a foreign LP cannot co-invest through a CIV regardless of their accredited investor status or SEBI eligibility. SEBI’s co-investment framework does not override FEMA restrictions. AIF managers structuring Shelf PPMs for CIV Schemes with a mixed domestic-foreign LP base must therefore build in explicit FEMA screening at the deal offer stage: before extending a co-investment invitation to foreign LPs, the manager must confirm that (i) FDI is permitted in the portfolio company’s sector, (ii) the applicable entry route is satisfied, and (iii) existing foreign investment in the portfolio company does not breach the sectoral cap when aggregated with the proposed CIV investment. Failing to do so creates FEMA contraventions at the portfolio company level, a liability that ultimately falls on the investee, not just the investor.

The January 2025 Master Direction Update: Structuring Relief for FOCCs

A welcome development relevant to foreign LP co-investment came with RBI’s updated Master Direction on Foreign Investment in India introduced on 20 January 2025. The update resolved longstanding ambiguity by expressly clarifying that payment arrangements available for direct FDI, including equity instrument swaps and deferred consideration mechanisms, are equally available for downstream investments by Foreign Owned and Controlled Companies (“FOCCs”). This is practically important for CIV structures: deal structuring in private markets often involves earnouts, deferred tranches, or share-swap elements. Prior to this clarification, FOCCs had taken a conservative approach and avoided such structures for downstream investments due to regulatory uncertainty. That uncertainty is now resolved, making FOCC-backed CIV co-investments structurally more flexible than they were even a year ago.

The Conclusion

With over INR 15.74 trillion in commitments and a sustained 30% CAGR, India’s AIF industry has outgrown its niche origins to become a cornerstone of the country’s capital markets architecture. The 2025 regulatory overhaul including the introduction of Co-investment Vehicle Schemes, Accredited Investor-only Schemes, and a streamlined accreditation framework signals SEBI’s intent to build a globally competitive, investor-sophisticated alternative capital ecosystem. The real test, however, remains whether this capital finds its way to startups and innovation-led sectors, rather than flowing overwhelmingly to safer late-stage bets. With only ~3.2% of AIF investments reaching startups as of December 2025, the industry’s response to that challenge and SEBI’s regulatory nudges to address it will define India’s AIF story in the decade ahead.

You can download this article here:

Contributors & Disclaimer

Authors: Souvik Ganguly and Jagannathan M

Research Assistant: Srividya M S

For any queries or further engagement on the matters discussed in this paper, please reach out to Acuity Law at [email protected].

The information contained in this document is not legal advice or legal opinion. The contents recorded in the said document are for informational purposes only and should not be used for commercial purposes. Acuity Law LLP disclaims all liability to any person for any loss or damage caused by errors or omissions, whether arising from negligence, accident, or any other cause.