IPO Preparation: A Structured Approach for Promoters

Introduction

An Initial Public Offering (IPO) represents one of the most significant milestones in a company’s lifecycle. It is not merely a fundraising exercise but a fundamental business transformation from a closely held enterprise into a regulated, disclosure driven and institutionally governed entity. For promoters, this transition demands meticulous preparation across legal, financial, governance and operational dimensions, often well before the formal process is initiated.

Successful IPOs are distinguished not by market timing alone, but by the depth and quality of groundwork laid by promoters in the months and years preceding the offering. This document presents a ten-stage structured framework for IPO preparation, distilled from practical execution experience, to guide promoters through each phase of the journey from an initial readiness assessment through to post listing compliance obligations.

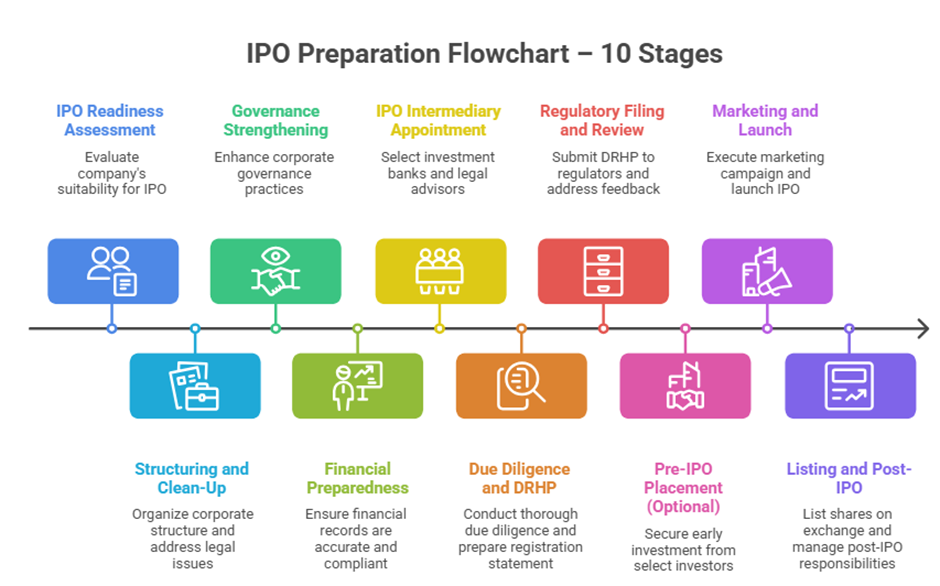

The flowchart below provides a visual overview of the ten stages, followed by a detailed explanation of each stage.

Stage 1: Assessment of IPO Readiness

Before even appointing advisors, promoters must evaluate whether the company is genuinely ready for an IPO. This is a foundational step that is often underestimated, yet it determines whether the entire process that follows will be smooth or fraught with obstacles.

This assessment involves a candid review of the company’s scale of operations, profitability track record, growth trajectory, positioning within its industry, and the visibility of future business prospects. Companies going public are expected to demonstrate consistent financial performance and a clear, credible business model not just a promising idea or a single good year.

At this stage, promoters should ask the following critical questions:

- Is the business scalable and sustainable?

- Are the financials stable and credible?

- Is there a strong second line of management capable of running the company independently?

- Is the Company eligible to make an Initial Public Offering under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018?

If gaps are identified at this stage, such as inconsistent profits, absence of proper systems and processes, or weak corporate governance, they must be addressed before moving forward to ensure that such reasons do not result in delays during the IPO approval process, or a weak market reception.

Stage 2: Structuring and Corporate Clean-Up

This is one of the most critical phases in IPO preparation and, in practice, one of the most time consuming. Many companies that have operated for years as private entities carry with them structural complexities, informal arrangements, and legacy issues that are entirely incompatible with the standards expected of a listed company.

The corporate clean up involves ensuring that the legal, financial, and organisational structure of the company is clean, compliant, and capable of withstanding public scrutiny. This specifically includes:

- Simplifying the group structure by removing unnecessary subsidiaries or related entities.

- Regularising related party transactions.

- Ensuring that all statutory filings are up to date.

- Cleaning up old disputes, litigations, or non-compliances that could become red flags in the prospectus.

Additionally, promoters must ensure proper documentation of all past transactions, clear and uncontested ownership of assets and intellectual property, and the elimination of any informal or undocumented arrangements between the company and promoters or related parties.

This stage builds the foundation for the due diligence exercise that will follow later in the process.

Stage 3: Strengthening Corporate Governance

A listed company is subject to significantly higher standards of governance than an unlisted one. Key governance actions that must be taken at this stage include:

- Appointment of a full-time Company Secretary and Compliance Officer.

- Appointment of a Chief Financial Officer with the appropriate qualifications and experience.

- Appointment of Senior Management personnel across key functions.

- Appointment of Independent Directors who bring credibility, expertise, and objectivity to the board.

- Formation of mandatory board committees, including the Audit Committee, Nomination and Remuneration Committee, Stakeholders Relationship Committee, and Corporate Social Responsibility Committee.

- Adoption of formal policies as required under the Companies Act, 2013 and the SEBI (Listing Obligations and Disclosure Requirements) Regulations.

Promoters must understand that decision making in a listed company will become more structured, and documented.

Stage 4: Financial Preparedness

Financial statements are the backbone of an IPO. Investors, analysts, and regulators will scrutinise the company’s financials in detail and depth. Any inconsistency, restatement, or qualification will raise doubts and potentially derail or delay the offering.

At this stage, the company must undertake the following:

- Prepare restated financial statements for the last three financial years and any stub period, as required under SEBI’s regulations.

- Ensure full compliance with applicable accounting standards.

- Strengthen internal financial controls.

- Resolve qualifications or remarks by the auditor.

Additionally, the company should look to improve working capital management cycles, align revenue recognition practices with applicable standards, and ensure that tax positions are well-documented and capable of being defended before the authorities. Consistency, transparency, and accuracy are the watchwords at this stage.

Stage 5: Appointment of IPO Intermediaries

Once the company has reached a reasonable state of preparedness, it is time to appoint the professional advisors. The key ones typically appointed include:

- Merchant Bankers (also referred to as Book Running Lead Managers or BRLMs) who play the central role in managing the entire IPO process, including valuation, drafting of the prospectus, regulatory filings, and investor outreach.

- Legal Counsel, both for the company and for the Merchant Bankers, or a sole legal counsel for the Company and Merchant Banker who shall conduct legal due diligence and ensure the accuracy and completeness of legal disclosures in the prospectus.

- Peer Reviewed Auditor who audits and certifies the restated financial statements included in the prospectus.

- Registrar to the Issue who manages the application process, allotment, and refunds.

- Other intermediaries such as public relations agencies, as required.

The Merchant Banker, in particular, is the driver of the IPO process. The Merchant Banker coordinates between all parties, managing the regulatory timeline, advising on valuation and pricing, and ensuring that the company is presented in the best possible light to investors.

Stage 6: Due Diligence and Documentation (DRHP Preparation)

This is the most detailed and intensive stage of the IPO process. Due diligence involves a thorough and systematic examination of every material aspect of the company’s business, and the findings are reflected in the Draft Red Herring Prospectus (DRHP), the primary disclosure document filed with the regulators and made available to investors.

The due diligence exercise covers all key aspects of the company’s business, including:

- Business model

- Financials

- Legal and Secretarial Matters

- Litigations and Government Approvals

- Board of Directors, Key Managerial Personnel and Senior Management

- Promoter and Promoter Group background

- Factory and Registered Office Visits

- Discussions between the Company, Merchant Bankers and Legal Counsels on the Objects of the Issue (Why the funds are being raised by the Company)

- Risks associated with the Industry in which the Company operates and with the Company.

Based on all of this, the DRHP is drafted. This is a voluminous and detailed document, and its preparation involves multiple rounds of review and revision between the company, the Merchant Bankers, and legal counsel. Promoters must provide complete and accurate information, respond promptly and thoroughly to queries from advisors, and ensure that all disclosures are transparent, balanced, and not misleading. The DRHP becomes the primary source of information for all investors and is a legally binding document.

Stage 7: Regulatory Filing and Review

Once the DRHP has been finalised and approved by the company’s board, it is filed with the Securities and Exchange Board of India (SEBI) and with the relevant stock exchanges, that is, in most cases, BSE Limited and the National Stock Exchange of India Limited.

SEBI and the Stock Exchanges undertake a detailed review of the DRHP from the perspective of investor protection. The regulators carefully examine the adequacy and accuracy of disclosures made in the DRHP, including the appropriateness of the Business, Objects of the Issue, the Risks related to the business of the Issuer Company, the Financials and the overall integrity of the document. SEBI and the Stock Exchanges may raise multiple rounds of queries and seek clarifications or additional disclosures.

Promoters should be prepared for:

Multiple rounds of detailed questions from SEBI and Stock Exchanges.

- Requirements to make additional disclosures or to modify existing disclosures to ensure greater clarity or accuracy.

- Clarifications on various chapters of the DRHP that may not have been adequately addressed in the initial filing.

This stage can take several weeks or even months, depending on the complexity of the company’s business and the nature of regulators observations. A well prepared DRHP will result in fewer queries and a faster resolution of the regulatory review process.

Post addressing the queries raised by the Stock Exchanges and Securities and Exchange Board of India, the Company receives final observations, pursuant to which it may proceed with the filing of the Red Herring Prospectus.

Stage 8: Pre-IPO Placement and Investor Readiness (Optional)

Some companies choose to raise funds through a pre-IPO private placement with institutional or strategic investors before the public offering. This can serve multiple purposes, such as, validating the company’s valuation, strengthening the balance sheet ahead of the IPO, and creating a base of informed and committed shareholders prior to listing.

Independently of any pre-IPO placement, promoters and senior management must also invest significant effort in preparing for investor engagement. This includes:

- Developing a compelling investor presentation that clearly articulates the company’s business, competitive strengths, financial track record, and growth strategy.

- Preparing for roadshows structured meetings and presentations with institutional investors, fund managers, and analysts in key financial centres.

- Rehearsing for analyst interactions and Q&A sessions, where management will be expected to answer detailed and sometimes challenging questions about the business.

The company’s story must be clearly and consistently articulated:

- What does the company do?

- How does it generate revenue and profit?

- What is the growth plan for the next three to five years?

- What is the specific purpose of the funds being raised, and how will their deployment benefit the company and, by extension, its future shareholders?

The quality of this narrative will have a direct impact on investor interest and the final pricing of the IPO.

Stage 9: Marketing and IPO Launch

Upon receipt of the final observations, the Company files the Updated Draft Red Herring Prospectus incorporating all comments, clarifications and revisions as required by the Stock Exchanges and Securities and Exchange Board of India.

Post receiving approval from the Regulators on the UDRHP, the most visible phase of the entire process, the moment when the company formally enters the public domain and invites investors to subscribe to its shares.

The key activities at this stage include:

- Price band determination the company, in consultation with the Merchant Bankers, decides the price range within which bids will be accepted from investors.

- Roadshows and investor meetings intensive and often back-to-back meetings with institutional investors in which senior management presents the company’s investment case.

- Filing of the Red Herring Prospectus and Opening of the issue for public subscription, typically for a period of three working days, during which investors from all categories can bid for shares.

During the subscription period, three categories of investors participate: Qualified Institutional Buyers (QIBs), Anchor Investors, and Individual Investors. Each category has a reserved portion of the issue.

Promoters and the Chief Financial Officer must be actively involved during this phase, meeting investors, participating in roadshows, and communicating the company’s vision, financial strength, and growth prospects with clarity, credibility, and confidence.

Stage 10: Listing and Post-IPO Responsibilities

After the subscription period closes and the issue is found to have been successfully subscribed, shares are allotted to investors and the company’s shares are listed and begin trading on the stock exchange. This marks the formal culmination of the IPO process but it is emphatically not the end of the journey.

Life as a listed company brings with it a continuous and demanding set of obligations. Post listing, the company must comply with:

- Quarterly and annual financial disclosures.

- Corporate governance requirements.

- Continuous disclosure obligations.

Promoters must adapt to an entirely new operating environment:

- Market scrutiny: The company’s performance, decisions, and even statements will be closely watched and commented upon by analysts, investors, and the financial media.

- Investor expectations: Shareholders will expect consistent execution against the plans and projections disclosed at the time of the IPO.

- Transparent communication: All material developments must be disclosed promptly and accurately, without selective or preferential sharing of information.

The discipline and rigour developed during the IPO preparation process serve promoters well in meeting these post-listing obligations. A company that has invested seriously in governance, compliance, and financial discipline during the pre-IPO phase will be well-equipped to meet the demands of public market scrutiny.

Conclusion

The path to a successful IPO is neither linear nor swift. Each of the ten stages outlined above carries its own set of complexities and requires the sustained attention of promoters, management, and professional advisors alike. Gaps identified at any stage, whether in governance structures, financial controls, regulatory compliance, or corporate documentation must be addressed proactively rather than deferred to the due diligence phase.

Promoters who invest in thorough preparation typically experience a smoother regulatory review, stronger investor confidence, and a more favourable reception in the capital markets. By contrast, companies that approach the IPO process reactively often face delays, additional regulatory scrutiny, and reputational risk that is difficult to repair once the offering is in the market.

Ultimately, listing on a stock exchange is not the end of the journey, it is the beginning of a new chapter governed by heightened accountability, transparency, and stakeholder expectations. The discipline of preparation instilled during the IPO process serves as the foundation for long-term success as a publicly listed company.

You can download this article here:

Contributors & Disclaimer

Authors: Souvik Ganguly and Mohit Parekh

Research Assistants: Juhi Parekh and Shivam Natani

For any queries or further engagement on the matters discussed in this paper, please reach out to Acuity Law at [email protected].

The information contained in this document is not legal advice or legal opinion. The contents recorded in the said document are for informational purposes only and should not be used for commercial purposes. Acuity Law LLP disclaims all liability to any person for any loss or damage caused by errors or omissions, whether arising from negligence, accident, or any other cause.