Jindal Equipment Leasing Consultancy Services Ltd v. CIT

Introduction:

In a landmark decision of Jindal Equipment Leasing v. CIT, the Supreme Court has observed that the inherent assumption of tax-neutrality under Section 47(vii) of the Income-tax Act, 1961 (“IT Act”) for share swaps during corporate amalgamations may not be correct. Such assumption would only be applicable to shares held as ‘capital asset’ by shareholder. The ruling established in principle that pursuant to a scheme of amalgamation, swap of shares initially held by shareholders as ‘stock-in-trade’, and not as ‘capital asset’, in the amalgamating company in lieu of shares in amalgamated company is taxable as ‘business income’ under Section 28 of the IT Act.

Consequently, this precludes the automatic application of the exemption under Section 47(vii) of the IT Act by presaging the taxpayer’s original classification of shares in amalgamating company, as a ‘capital asset’ or ‘stock-in-trade’, as the decisive factor for determining tax incidence in corporate amalgamations.

Brief Facts:

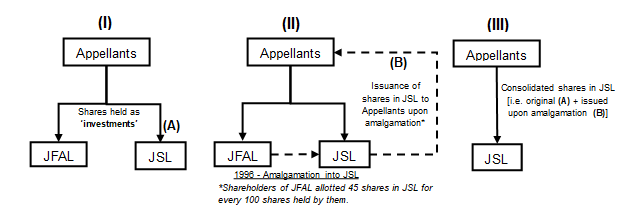

Jindal Equipment Leasing Consultancy Services Ltd., M/S Nalwa Investment Ltd., M/S Abhinandan Tradex Ltd. And M/S Mansarover Tradex Ltd. (collectively referred to as the “Appellants”) are investment companies holding shares in Jindal Ferro Alloys Limited (“JFAL”) and Jindal Strips Limited (“JSL”). Appellants hold shares in JFAL and JSL as a part of the promoter holding thereof, representing controlling interest. These shares were reflected as “investments” in the respective balance sheets of the Appellants.

A scheme of amalgamation (‘Scheme’) was entered into under which JFAL was amalgamated with JSL. The effective date of the amalgamation was 22 November 1996. Pursuant to the Scheme, the shareholders of JFAL were allotted 45 shares in JSL for every 100 shares of JFAL held by them.

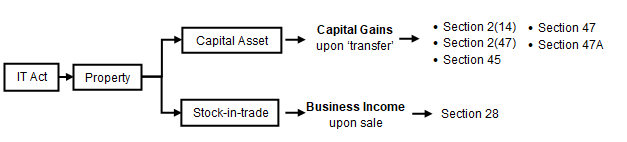

Under the provisions of Income-tax Act, 1961 (“IT Act”), any ‘transfer’ (as defined in Section 2(47) of IT Act1) of capital asset would trigger capital gains tax incidence in hands of seller of such capital asset in the year of ‘transfer’ thereof. Shares are also treated as capital asset. However, there are certain transactions which are not regarded as ‘transfer’ and Section 47 deals with ‘Transactions not regarded as transfer’. Section 47(vii) provides that any transfer by shareholder in a scheme of amalgamation of capital asset being shares held in amalgamating company, shall not be regarded as ‘transfer’ if such transfer is made in consideration of allotment of shares in amalgamated company being an Indian company. Accordingly, in respect of transfer of shares in JFAL in lieu of allotment of shares in JSL under the Scheme, Appellants claimed exemption under Section 47(vii) for Assessment Year 1997-98.

| Order by | What was held? |

| Assessing Officer (“Revenue”) (29 February 2000) | Treated the shares held in JFAL by Appellants as ‘stock-in-trade’ and denied exemption under Section 47(vii) In the absence of ‘capital asset’ classification, the transaction was treated as ‘business income’ with the value of JSL shares being taxed as business income computed with their market value. |

| Appeal before | Appeal preferred by | What was held? | Judgement in favour of? |

| CIT(Appeals) | Appellant | Upheld the Revenue’s order stating that the shares held in JFAL were in nature of stock-in-trade and since it is the same group, it is a scheme for profit-making by exchange of shares hence taxable under Section 28 of IT Act2 | Revenue |

| Tribunal (17 February 2005) | Appellant | Favoured the Appellants It is not necessary to decide whether the shares are held as ‘stock in trade’ or ‘capital assets’ No profit accrued unless the shares held are either sold or transferred No transfer of shares happened when the shares in JSL were allotted and hence no taxable profit Dismissed Revenue’s contentions | Appellant |

| Delhi High Court (“High Court”) (7 August 2020) | Revenue | Favoured the Revenue The questions before the High Court were: Whether the shares received by the Appellants on amalgamation are entitled to the benefit of section 47 (vii) without the Tribunal concluding that the said shares were held as capital assets? Whether the benefit of Section 47(vii) is limited to determination of capital gains and only regarding capital assets? Whether income would accrue to the Appellants’ on shares received by amalgamations and will be taxable in view of non-applicability of Section 47(vii)? If shares of the amalgamating company (JFAL) were held as ‘capital assets’ then it would constitute a ‘transfer’ under Section 2(47) of the IT Act. Accordingly, claiming exemption from ‘transfer’ u/s 47(vii) may be in order. If it was held as stock-in-trade, and not capital asset, then it would be taxable as business profit under Section 28 of IT Act. The capital gain provision would not apply to such stock-in-trade. Matter was remanded back to Tribunal for determination of nature of holding i.e. whether ‘capital assets’ or ‘stock-in-trade’ | Revenue |

| Supreme Court | Appellants | Appealed before the Supreme Court contending that: the appeals before the High Court did not include the question of taxability of receipt of shares of the amalgamated company as stock in trade. Thus, the High Court exceeded its scope under this appeal; the receipt of shares of the amalgamated company does not amount to either a “sale” or an “exchange”; taxable income arises only when real income accrues from the actual sale of the shares in the amalgamated entity. An analysis of the decision of the Supreme Court on the above contentions raised by the Appellants can be found below. | Revenue |

Tax framework:

Section 45 deals with the taxation of ‘Capital Gains’. It provides that profits or gains from transferring a capital asset during the previous year are chargeable to income-tax under the head “Capital gains”. Section 2(14) of the IT Act defines ‘capital asset’ to mean property of any kind held by a person. Shares in a company are treated as “property” and hence as a “capital asset”. However, ‘capital asset’ does not include “stock-in-trade” held for the purposes of business or profession.

Section 47 provides for exemption from definition of ‘transfer’ covering, amongst other things,

“…47(iv) Transfer of a capital asset from a company to its subsidiary if the parent company…holds 100% of the subsidiary’s share capital, and the subsidiary is an Indian company

47(v) Transfer of a capital asset from a subsidiary company to its holding company if the holding company holds 100% of the subsidiary’s share capital, and the holding company is an Indian company.

47(vi) any transfer, in a scheme of amalgamation, of a capital asset by the amalgamating company to the amalgamated company if the amalgamated company is an Indian company;

47(vii) any transfer by a shareholder, in a scheme of amalgamation, of a capital asset being a share or shares held by him in the amalgamating company, if—

- the transfer is made in consideration of the allotment to him of any share or shares in the amalgamated company except where the shareholder itself is the amalgamated company, and

- the amalgamated company is an Indian company…”

Further, Section 47A provides for withdrawal of such exemption in 47(iv) and (v) in case the transferee company converts the capital asset into stock-in-trade of its business.

Upon such conversion, profits or gains arising from the transfer of that capital asset, which were not taxed under section 45 because of the provisions of clause (iv) or clause (v) of section 47, shall, be regarded as income under the head “Capital gains” of the previous year in which such transfer took place.

Accordingly, the provisions of Section 47 envisage exemption from ‘transfer’ w.r.t ‘capital assets’.

Appellants’ submissions:

The Appellants contended that:

- The High Court exceeded its jurisdiction under Section 260A of the IT Act3 by introducing new questions. According to them, the only issue before the Court was whether the Tribunal was correct in holding that no transfer takes place when a taxpayer receives shares of the amalgamated company in lieu of shares of the amalgamating company.

- They further argued that the receipt of shares pursuant to amalgamation does not amount to a sale or exchange, as the shares of the amalgamating company cease to exist. Consequently, no exchange occurs and no taxable business income arises.

- It was also submitted that the definition of “transfer” under Section 2(47) applies only to capital gains and not to stock-in-trade.

- Illusory benefits cannot be taxed, and real income would arise only upon the actual sale of the allotted shares, not at the stage of allotment in lieu of extinguishment of shares in amalgamating company.

Revenue’s submissions:

The Revenue argued that:

- the core issue is not whether a transfer occurred, but whether business income arose.

- Section 28, unlike Section 45, does not require a transfer for income to be taxable as business income.

- Actual realisation of income is not necessary, as income accrues when it becomes due and when there is a corresponding liability on the other party, placing reliance on the decision in Excel Industries4.

Supreme Court ruling : Further to the Delhi High Court Ruling in favour of the Revenue, the Appellants preferred an appeal before the Supreme Court. The Supreme Court held that:

- Charging Provision and Exemption under the IT Act: Only a transaction that falls within a charging provision of the IT Act can be subjected to tax, and it is only after such taxability is established that the question of exemption arises. Accordingly, the transfer of shares pursuant to an order of amalgamation, even if treated as involving a capital asset, would ordinarily attract tax. Section 47(vii) of IT Act does not negate the existence of a taxable event but operates to exempt such transfer from taxation where the statutory conditions prescribed therein are satisfied.

- Where the shares of an amalgamating company, held as stock-in-trade, are substituted by shares of the amalgamated company pursuant to a scheme of amalgamation, and such shares are realisable in money and capable of definite valuation, the substitution gives rise to taxable business income within the meaning of Section 28 of the IT Act. The charge under Section 28 is, however, attracted only upon the allotment of new shares.

- Scope of Section 28 of IT Act – Business Income: The ambit of Section 28 is wide and is designed to bring within the tax net all real profits and gains arising in the course of business. Business income may accrue or be realised in diverse situations, even in the absence of a conventional sale, transfer, or exchange in the strict legal sense.

- Amalgamation, as a statutory substitution, ensures continuity of enterprise but also extinguishes one form of holding and replaces it with another. As we have held, where such substitution confers on the taxpayer realisable assets of definite market value, a commercial realisation takes place, and Section 28 is attracted. At the same time, courts must remain alive to the distinction between genuine commercial gain and hypothetical accretion. The touchstone is, therefore, the doctrine of real income, applied with due regard to the facts of each case, ensuring that the tax charge operates neither oppressively nor evasively, but in harmony with the legislative design, to tax true profits of business, however manifested, while eschewing illusory gains.

- Receipt or Accrual of Income upon Amalgamation: Where a taxpayer holds shares of the amalgamating company as stock-in-trade and, pursuant to an amalgamation, receives shares of the amalgamated company in substitution, there is, in substance, a receipt of consideration in kind. Such receipt constitutes the accrual of income for the purposes of business taxation, subject to the principles governing commercial realisation.

- Commercial Realisation as the Governing Test: The true test under Section 28 is not the legal characterisation of the transaction as an ‘exchange’ or ‘transfer’, but whether the taxpayer has, in consequence of the amalgamation and in the course of its business, obtained a profit that is real and presently realisable. The focus is on commercial substance rather than legal form.

- The assessment of commercial realisation depends on three cumulative factors: (a) the old stock-in-trade has ceased to exist in the taxpayer’s books; (b) the shares received in the amalgamated company possess a definite and ascertainable value; and (c) the taxpayer is in a position, immediately upon allotment, to dispose of such shares and realise money. These conditions i.e. actual receipt, present realisability, and ascertainability of value-together determine the timing of taxability in cases of amalgamation.

- The taxable event depends on the substance of the transaction and not merely accounting entries. Whether the shares are held only as investment, is a matter requiring factual determination and the same is remitted back to the Tribunal for fresh adjudication in accordance with law.

Our thoughts:

The Supreme Court, through this judgement, has clarified that mergers involve more than a simple substitution of one company’s shares for another’s. The Supreme Court has upheld that the accounting treatment or asset classification for equity investments in the hands of shareholder may be a key factor in determining consequential tax treatment under IT Act in cases involving amalgamations. For shareholders treating shares in amalgamating as stock-in-trade, this cannot qualify as a continuation of investment and the consequential receipt of fresh shares in amalgamated company pursuant to such amalgamation, would be taxable as business income. The judgement effectively dismantles the presumption of blanket tax neutrality for merger participants, even if statutory conditions under the IT Act are met. The test of ‘capital asset’ v/s stock-in-trade becomes paramount prior to determining taxable event. Accordingly, it is imperative that parties to a corporate restructuring exercise duly ensure such accounting treatment in their books in order to avail benefits under Section 47(vii).

The information contained in this document is not legal advice or legal opinion. The contents recorded in the said document are for informational purposes only and should not be used for commercial purposes. Acuity Law LLP disclaims all liability to any person for any loss or damage caused by errors or omissions, whether arising from negligence, accident, or any other cause.

- Transfer under Section 2(47) in relation to a capital asset includes, among other things, sale, extinguishment, relinquishment of such asset and also extinguishment of any rights therein ↩︎

- Section 28 of IT Act deals with computation of business income ↩︎

- Section 260 A of the Income Tax Act, 1961 provides that an appeal shall lie to the High Court from every order passed by the Appellate Tribunal, if the High Court is satisfied that the case involves a substantial question of law. ↩︎

- (2013) 358 ITR 295 (SC) – The judgement states that income accrues when there is a vested right to receive it and a corresponding liability on the other party ↩︎